Tokyo Office Vacancy at 2.20%: a Golden Age for Landlords, a Nightmare for Tenants

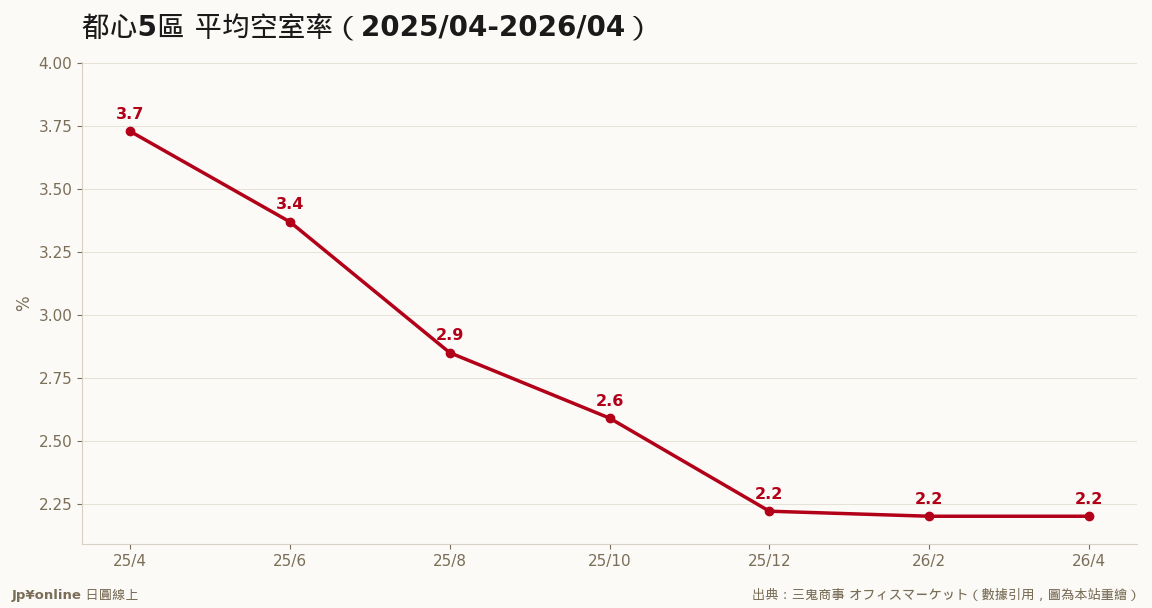

- April 2026 vacancy in Tokyo's central 5 wards: 2.20%, down from 3.73% a year ago (Miki Shoji)

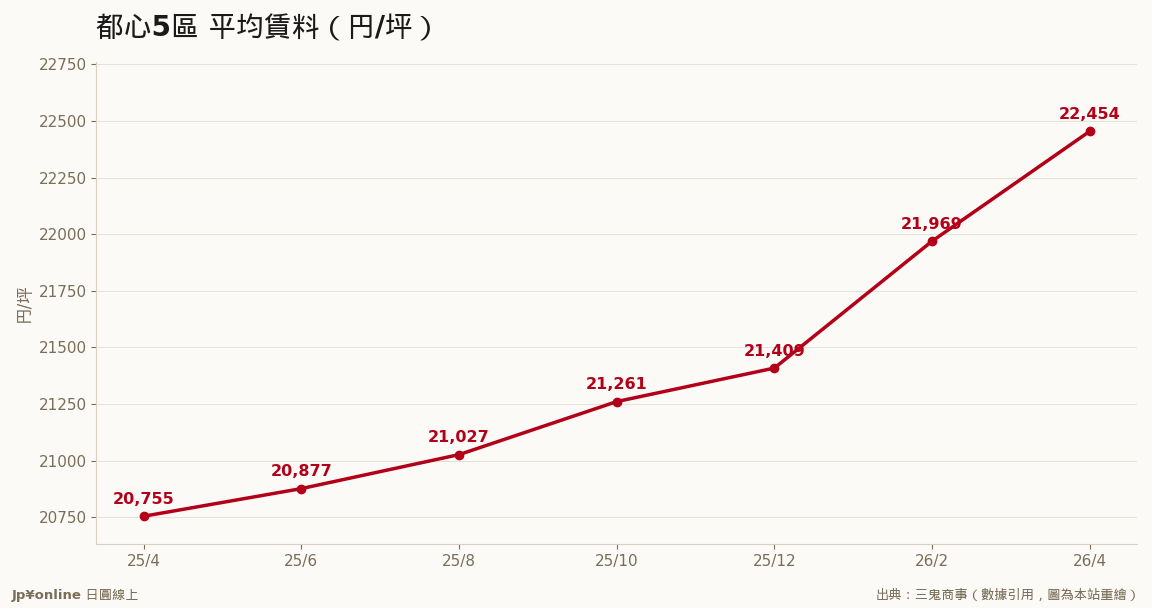

- Average rent ¥22,454/tsubo, up 8.19% YoY — rents accelerate once vacancy breaks 3%

- Tightest: Chiyoda 1.42%, Shibuya 1.39%; Shibuya rents top at ¥25,124/tsubo

- 5% is equilibrium, 2% is effectively full — Tokyo is flying at the limit

A year ago 3.73% of central Tokyo offices sat empty; now it's 2.20%. In twelve months the market buried the post-pandemic 'office glut' thesis. Remote work didn't kill the office — it killed the bad office.

Tokyo's office market has moved from recovery to squeeze: 2.20% vacancy is statistically full, and 8% rent growth is just the opening act. Sweet if you hold J-REITs; a cost alarm if you're opening a Tokyo office.

The coordinates: 5% vacancy is equilibrium, 2% is effectively full because transition vacancy alone accounts for that much. Miki Shoji's April reading of 2.20% — down from 3.73% a year ago — is the fastest absorption since early Abenomics.

Why are offices scarce in the remote-work era? A quality run: Japanese firms didn't shrink their footprint, they migrated en masse from old buildings to new ones, driven by the HR arms race for talent and expanding tech tenants. Shibuya proves it: the lowest vacancy (1.39%) and highest rent (¥25,124/tsubo) in the core. New buildings fill within months of completion.

Below 3% vacancy, rent physics change from drift to acceleration — landlords know tenants have nowhere to go. Expect renewal-shock headlines as leases roll over.

Two angles for Taiwanese readers: J-REITs and office developers have hard-data rent growth (8% nominal against 3% inflation is real growth); and if you're opening in Tokyo, your bargaining position is the worst in a decade — budget loose, decide fast, or put back-office functions in Yokohama or Omiya and keep only the storefront downtown.