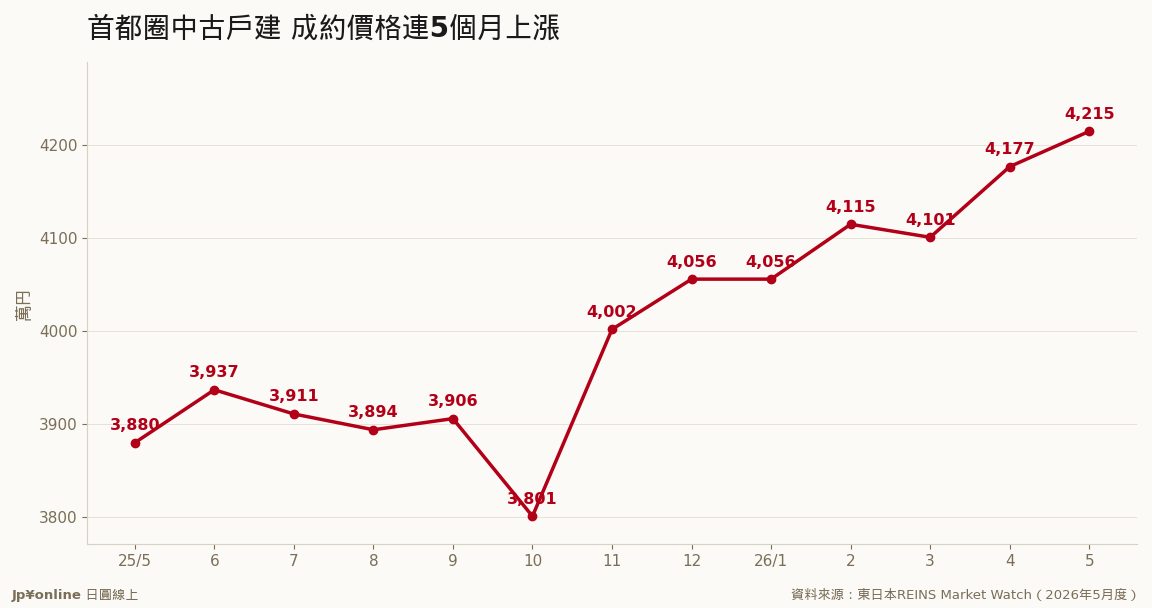

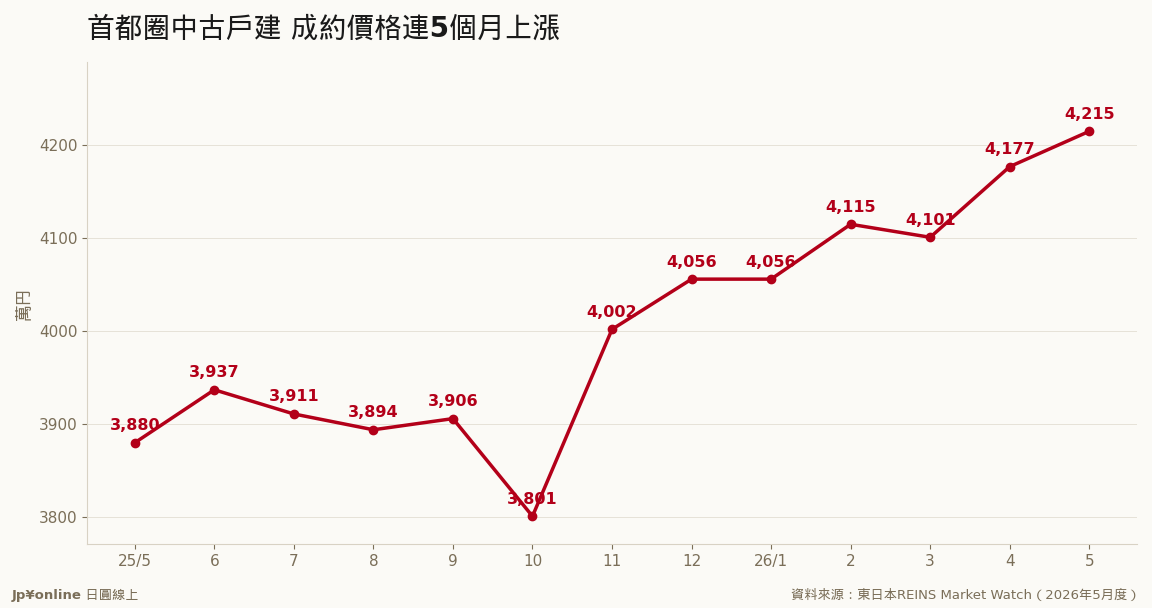

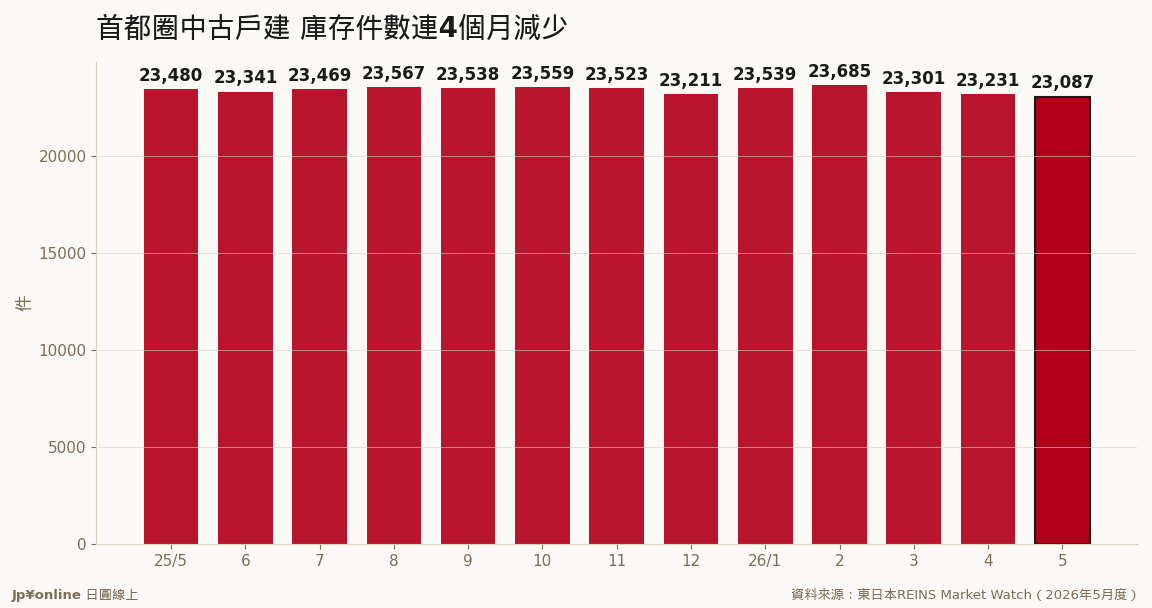

Condos Fall, Houses Rise: Tokyo-Area Used Detached Homes Up 8.7% for a Fifth Straight Month

- Average contract price reached 42.15 million yen, up 8.7% YoY, rising for five consecutive months

- Transactions grew 2.9% YoY to 1,835 units, a second straight monthly increase

- Inventory fell 1.7% YoY to 23,087 units, declining four months in a row — the mirror image of condos

- Contracted land area expanded 3.8% YoY to 151.19 sqm, buyers paying more for more land

Same region, same month, opposite script. While Tokyo-area used condominiums posted their first price decline in 73 months, used detached houses went the other way in REINS's May data: average contract prices hit 42.15 million yen, up 8.7% year-on-year and rising for a fifth straight month; transactions grew 2.9% to 1,835 units; and inventory fell 1.7% to 23,087 units, its fourth consecutive decline. Rising prices, rising volume, shrinking inventory — three indicators pointing the same direction, a mirror image of the condo market. Contracted land area expanded 3.8% to 151.19 square meters, meaning buyers are paying more and getting more land, not trading down. The most plausible driver is relative value: condos now close at an average 50.67 million yen versus 42.15 million for houses, with condo unit prices at bubble-era levels. When apartments become unchaseable, budget-conscious owner-occupiers pivot to houses that come with land. New house listings fell 0.9%, a fourth straight decline, so supply is tightening too. Caveats: the detached market is half the condo market's size and last year's base saw 60%-plus swings, so monthly noise runs hotter. But the signal stands — Tokyo housing demand has not disappeared; it has changed lanes.

Detached house prices climbed from a low of 38.01 million yen in October 2025 to 42.15 million in May 2026, up 8.7% year-on-year and rising for five straight months — a sharp contrast with condo prices turning down the same month.

Inventory has slid month by month from its February peak of 23,685 units to 23,087, down four consecutive months on an annual basis, while new listings also fell for a fourth month. Demand up, supply down — prices have support. With condo inventory rising three months running, the rotation from pricey condos to land-attached houses shows up clearly in the data.